2023 Income Limits if You and/or Your Spouse Also Have a Retirement Account from Your Employer

Retirement accounts contain money that you have set aside to use once you are retired. What makes these accounts different from other investments is that the federal government allows them to grow tax-free. However, you do not have easy access to the money when you are younger.

Retirement accounts contain money that you have set aside to use once you are retired. What makes these accounts different from other investments is that the federal government allows them to grow tax-free. However, you do not have easy access to the money when you are younger.

The Employee Retirement Income Security Act (ERISA) of 1974 sets the rules for retirement accounts that protects them, including from creditors, and allows you to receive tax benefits.

Once funded, the account then earns tax-deferred gains. The sacrifice for this is that you can’t withdraw untaxed contributions before 59½ years old without penalty and the federal government sets yearly limits on how much can be added to each type of account. Your employer may set their own limits on how much you can contribute, either a dollar amount or percent of your salary.

Like annuities, most retirement accounts have a limit on how long you can defer withdrawals. The limit is 73 years old (70½ if you turned that age before 2020) or age of retirement, whichever is older. The Roth IRA is an exception and has no minimum age requirements to start distributions.

Once funded, the account then earns tax-deferred gains. The sacrifice for this is that you can’t withdraw untaxed contributions before 59½ years old without penalty and the federal government sets yearly limits on how much can be added to each type of account. Your employer may set their own limits on how much you can contribute, either a dollar amount or percent of your salary.

Like annuities, most retirement accounts have a limit on how long you can defer withdrawals. The limit is 73 years old (70½ if you turned that age before 2020) or age of retirement, whichever is older. The Roth IRA is an exception and has no minimum age requirements to start distributions.

- At that point you must begin taking required minimum distributions (RMDs).

- RMDs are based on the value of your investments, age, and expected lifespan according to the Internal Revenue Service (IRS) life expectancy table.

- RMDs are initially 4% of your account’s balance and increase with age.

- This means that as you get older you must withdraw increasingly larger percentages of your account balance.

- A RMD calculator and detailed information about RMDs can be found on the AARP website.

- For each year you defer after that you will pay an excise tax penalty equal to 50% of the amount you should have withdrawn.

- All of the withdrawal from 401(k), 403(b), 457(b), profit-sharing plans, and traditional IRA (Individual Retirement Accounts) accounts is taxed as income, since it was funded by pre-tax dollars.

- Only the gains are taxed on withdrawals from Roth versions of these accounts, since they were funded by after-tax dollars

Many retirement plans are sponsored by employers and allow you to contribute pre-tax or after-tax dollars. In some cases, the employer may match some or all of your contributions. Employers can receive up to $500 of tax credit per year if they create a 401(k) or SIMPLE IRA plan with automatic enrollment.

Many retirement plans are sponsored by employers and allow you to contribute pre-tax or after-tax dollars. In some cases, the employer may match some or all of your contributions. Employers can receive up to $500 of tax credit per year if they create a 401(k) or SIMPLE IRA plan with automatic enrollment.

If your employer offers them, they are available to full-time and part-time employees who work either 1,000 hours per year or have worked three consecutive years with at least 500 hours. You can only make deposits with funds from your salary.

Depending on the type of account, there are three types of contributions.

- Elective deferrals – pre-tax contributions you have taken out of your salary which are contributed directly into the account for your benefit.

- Non-elective contributions – untaxed contributions by your employer to your account, such as matching contributions, discretionary contributions, and mandatory contributions.

- After-tax contributions – contributions to Roth accounts or additional contributions you can make if your plan allows them.

Within the federal limit and any limit set by your employer, you can choose how much to deposit.

Some employers will match some or all of your contributions and get tax relief for them.

- Most will have a limit, which may or may not be the same as your contribution limit.

- Because of higher budgets, for-profit companies are more likely to match contributions, while non-profit companies with lower budgets are less likely to match contributions.

- Employers that provide employees a pension, such as for police officers, firefighters, other civil servants, ministers, school administrators, state college professors, and teachers will usually not match contributions.

While you are entitled to all of your contribution if you leave your job, you will not be entitled to all of your employer’s contribution until you are fully vested.

- Vesting indicates the percentage of your employer’s contribution you are entitled to.

- Vesting is usually tied to how long you have been employed.

- You will usually have to wait for full vesting with a 401(k). You should check with your employer about their vesting policy.

- You are usually fully vested as soon as you open a 403(b), which is offered by the government or non-profit organizations or you are employed in a business with less than 100 employees that offer a SAFE retirement plan or Safe Harbor 401(k).

- The Employee Retirement Income Security Act (ERISA) puts limits on the length of the vesting period.

If you change jobs you can either keep the account with your previous employer, move it, or cash it out. It can be difficult to choose among the options, but the decision is ultimately a financial one. You will be trying to balance the cost of services (fees) for moving the money with the possibility of making them up with a better return on your new account or investments.

If you change jobs you can either keep the account with your previous employer, move it, or cash it out. It can be difficult to choose among the options, but the decision is ultimately a financial one. You will be trying to balance the cost of services (fees) for moving the money with the possibility of making them up with a better return on your new account or investments.

- Your employer may require you to take your money out of their account or only allow you to stay in the account if you have a certain amount invested, but you cannot add additional funds.

- If desired or necessary, you can roll it over into an IRA. This may give you more choices such as lower fees, more control, or payment options.

- Some new employers will allow you to move the funds into the account they offer.

- You can cash it out, but you will lose the benefits of the account and usually pay surrender and service fees.

Employer retirement accounts can be qualified or non-qualified depending on whether or not they follow ERISA rules.

- Qualified retirement accounts like 401(k)s are those that are subject to all ERISA rules, such as tax-deferral, contribution limits, and when withdrawals can start without penalty.

- Non-qualified retirement accounts may not adhere to all ERISA rules, such as nondiscrimination rules.

- 403(b)s and 457(b)s have the same limits on contributions and withdrawal rules, but may not follow other rules and are usually considered non-qualified. This is especially true if your employer does not have a matching contribution program.

- 457(f)s are also non-qualified and do not have a limit on how much can be put into the account. They may be offered if you are a high-salaried employee.

The nondiscrimination rules in the ERISA assure that all employees of the company are eligible for the same benefits, no matter their position within the company.

- This keeps plans from for-profit companies (401ks) from treating highly-compensated employees and company executives differently when it comes to employer contributions.

- Plans from non-profit companies or governments (403b and 457b) are not usually at risk for this and are exempt from these rules.

- Companies that do not match contributions are also exempt from nondiscrimination rules.

If your adjusted gross income falls below a certain limit you may be eligible to take a non-refundable savers tax credit of up to $1,000 ($2,000 if married filing jointly) if you contributed to any type of employer-sponsored retirement plan.

Certificates of Deposit (CDs) are securities issued by commercial banks and pay a preset rate of interest over the term of the agreement. The Federal Deposit Insurance Corporation (FDIC) often acts as a guarantor of these securities. This oversight makes CDs relatively low-risk.

Certificates of Deposit (CDs) are securities issued by commercial banks and pay a preset rate of interest over the term of the agreement. The Federal Deposit Insurance Corporation (FDIC) often acts as a guarantor of these securities. This oversight makes CDs relatively low-risk.

Money Market Funds invest in short-term (typically less than one year) securities commonly traded in the money market. While there may be some capital gains, most of the gains in value come from interest.

Mutual funds are a managed portfolio of investments with money from various investors that is pooled and invested in a variety of different financial securities including stocks and bonds.

- Rather than purchase shares of an individual stock, the manager of the 401(k) buys shares of a mutual fund.

- These transactions are handled by the mutual fund manager or through a broker, rather than on an open market (exchanges).

Exchange-traded funds are a type of security similar to mutual funds. The investments usually involve a collection of securities such as stocks, but can also be invested in any number of industry sectors or use various strategies. Unlike mutual funds, exchange-traded funds are listed on exchanges and the shares trade throughout the day just like ordinary stock.

U.S. Treasury Bonds (T-bonds) provide you or your 401(k) with steady interest income, usually every 6 months. It is important to know that you must hold the bond through to maturity, usually 20-30 years, to earn a bond’s full yield.

Corporate Bonds provide recurring interest income, but unlike the U.S. Bonds there is risk involved that varies significantly by the issuer. Your 401(k) manager needs to conduct a thorough review of any corporate bond security before investing directly or through a mutual fund.

Annuities are becoming more common after the 2019 SECURE Act reduced liabilities for companies offering retirement plans.

401(k)s retirement plans are only available from your employer. If you work for a for-profit company, a 401(k) is the only retirement account of this type available. Some non-profit employers offer them, but it is less common.

401(k)s retirement plans are only available from your employer. If you work for a for-profit company, a 401(k) is the only retirement account of this type available. Some non-profit employers offer them, but it is less common.

Eligible employees can make tax-deferred contributions from their salary/wages on a post-tax (Roth) and/or pre-tax (traditional) basis. Employers may make matching or non-elective contributions to the plan and may also add a profit-sharing feature.

401(k)s from for-profit companies are more likely to be administered by mutual funds companies and to match some or all of your contributions.

Whether contributions are taken out before taxes (gross salary) or after taxes (take home salary) depends on which of the two types, traditional or Roth, you have. You may or may not have a choice of which one.

403(b) plans can only be offered by the government or non-profit organizations, such as a public education institution, religious organization, or 501(c)(3) Tax-Exempt Organization.

403(b) plans can only be offered by the government or non-profit organizations, such as a public education institution, religious organization, or 501(c)(3) Tax-Exempt Organization.

- They are more likely to be administered by insurance companies.

- 403(b)s offer a much more limited range of investment options, usually only mutual funds and annuities. This is usually to avoid high-risk investments.

- Eligible employees may make contributions from their salary/wages on a post-tax or pre-tax/tax deferred basis.

- Organizations that offer 403(b)s can, but are less likely to match contributions.

- 403(bs) are exempt from many Employee Retirement Income Security Act (ERISA) rules, especially if they do not match contributions.

Like a 403(b), a 457(b):

- Usually only invests in mutual funds and annuities; and

- Is offered by organizations that are less likely to match contributions; more so since 457 (b) plans are usually offered by organizations that have pension plans for retired employees such as police officers, firefighters, or other civil servants.

There are a number of differences from a 401(k) and 403(b).

There are a number of differences from a 401(k) and 403(b).

- There is no combined annual contribution limit, any contributions from your employer reduce what you can contribute by that amount. This is rarely a limited since most government employers do not offer to match contributions.

- In your final three years before retirement, you can contribute the lesser of:

- Twice the annual limit, up to $45,000 a year in 2023; or

- The basic annual limit plus the amount of the basic limit not used in prior years (only allowed if not using age 50 or over catch-up contributions).

- As long as you don’t exceed the $22,500 limit in the year 2023, you can contribute up to 100% of your salary.

- If you do not take advantage the 50 or over catch-up option, you can resort to unused contribution rollovers.

- These allow you to add any amount below the limit that you did not contribute last year to this year’s contribution.

- For example, if you only contributed $12,000 to your 457(b) plan in 2021 ($7,000 under the 2021 limit), you can contribute up to $27,500 in 2022 ($7,000 + $20,500).

- You won’t pay a 10% penalty fee if you withdraw money after leaving your job or retire before 59½ years old.

- Your money is not protected from creditors.

You can have a 457(b) and a 403(b) (or rarely a 401k) at the same time and be able to contribute up to the limit for both.

A profit-sharing plan is a retirement plan created for you but funded solely by your company. Also known as a deferred profit-sharing plan, it allows you to receive a percentage of your company’s profits based on its earnings. Any size company can set one up.

A profit-sharing plan is a retirement plan created for you but funded solely by your company. Also known as a deferred profit-sharing plan, it allows you to receive a percentage of your company’s profits based on its earnings. Any size company can set one up.

- The company decides how much of their profits they want to share and then determines what they allocate to you.

- Contributions amounts can be a percentage of your salary or determined by a formula based on your salary and your company’s earnings for that quarter.

- The amount of your salary will be used to calculate what percentage of the company’s total salary payments is yours.

- The amount of your salary that can be considered for a profit-sharing plan is limited, $330,000 in 2023.

- That number is then multiplied by the total profits being shared, if any.

- They are typically added to your account quarterly or annually.

- Once funded, the account grows tax-deferred like the other retirement accounts.

- Like all non-Roth accounts, the withdrawals are taxed as income.

- The company has all the control, but there are some rules they need to follow.

- The 2023 contribution limit for your company is the lesser of 100% of your salary or $66,000 ($73,500 for those 50 years old or older).

- Companies have to follow nondiscrimination rules, in other words the profit-sharing plan cannot discriminate in favor of highly compensated employees.

- Like other retirement plans, you will pay a 10% penalty for any funds you withdraw from the account before 59½ years old.

- After leaving the company, you can transfer the money into a traditional IRA without penalty.

- Profit-sharing plans usually have a vesting schedule that determines how long you have to work for your company before you are entitled to the full amount.

- A profit-sharing plan does not restrict the company from also offering a 401(k).

- You can take your funds in the form of cash or company stock.

A Savings Incentive Match Plan for Employees (SIMPLE) IRA is a savings plan available to small businesses with fewer than 100 who earn more than $5,000 per year and do not offer another retirement plan. To allow for growth of a business, the employer can still offer the plan for two years after the company exceeds 100 employees, after which they need to switch to a standard IRA plan.

A Savings Incentive Match Plan for Employees (SIMPLE) IRA is a savings plan available to small businesses with fewer than 100 who earn more than $5,000 per year and do not offer another retirement plan. To allow for growth of a business, the employer can still offer the plan for two years after the company exceeds 100 employees, after which they need to switch to a standard IRA plan.

IRS rules prohibit your company from offering you other types of retirement plans if you are covered by a SIMPLE IRA.

SIMPLE IRAs do not require non-discrimination rules, creation of vesting schedules, or tax reporting at the plan level; they are easier and less expensive to set up and manage than the previously described traditional plans.

Since businesses must match workers’ contributions to the plan, the SECURE Act gives them tax incentives to set it up. This tax credit is in addition to the 50% of necessary eligible start-up costs credit they already receive, up to a maximum of $500 per year for the first three years of the plan.

The plan allows pre-tax contributions by both employees and employers. The amount of possible savings is less than other types of plans.

A Simplified Employee Pension (SEP) plan or 408(k) plan gives employers the ability to contribute to traditional IRAs (SEP-IRAs) set up for employees.

A Simplified Employee Pension (SEP) plan or 408(k) plan gives employers the ability to contribute to traditional IRAs (SEP-IRAs) set up for employees.

An SEP plan has lower start-up and operating costs than conventional retirement plans, but is much different than a SIMPLE IRA. It is like a traditional IRA that your employer contributes to.

- It is designed for self-employed and small businesses, but is available for any size business.

- To qualify to participate you must at least be 21 years old, have three years of employment within the last five years, and earn at least $750 compensation per year.

- Participation in traditional IRAs and Roth IRAs does not disqualify you from participating.

- You may be disqualified if you are covered in a union agreement that bargains for retirement benefits or are a nonresident alien that does not receive U.S. wages or other service compensation from your employer.

- Only the employer makes contributions, not you or other employees. There are two exceptions.

- You can contribute to a Salary Reduction Simplified Employee Pension Plans created before 1997. However, elective salary deferrals or catch-up contributions are no longer allowed.

- If you are self-employed, you can contribute up to 20% of your net self-employment earnings towards your account.

- The contributions can vary from year to year based on how well the company is doing.

- Although there may be no contributions some years, the maximum can be higher than other retirement plans.

- In 2023, your employer can make contributions up to $66,000 or 25% of your net earnings from self-employment up to $330,000, whichever is lower.

- The funds are usually put into traditional IRAs, known as SEP-IRAs, set up for each eligible employee and are taxed accordingly.

- There are a variety of investment choices, but it is the IRA trustee that chooses the investments and you who make specific investment decisions.

- You are always 100% vested in the account and will receive the full amount when you leave, whenever that is.

- You cannot take loans from the account.

- Like other accounts, if you withdraw money before 59½ years old, you will pay a 10% early withdrawal penalty on the taxable portion of the money and you must begin minimum withdrawals before 73 years old (70½ if you turned that age before 2020).

- Contributions and earnings may be transferred over tax-free to other individual retirement accounts and retirement plans and must eventually be distributed following the IRA-required minimum distributions.

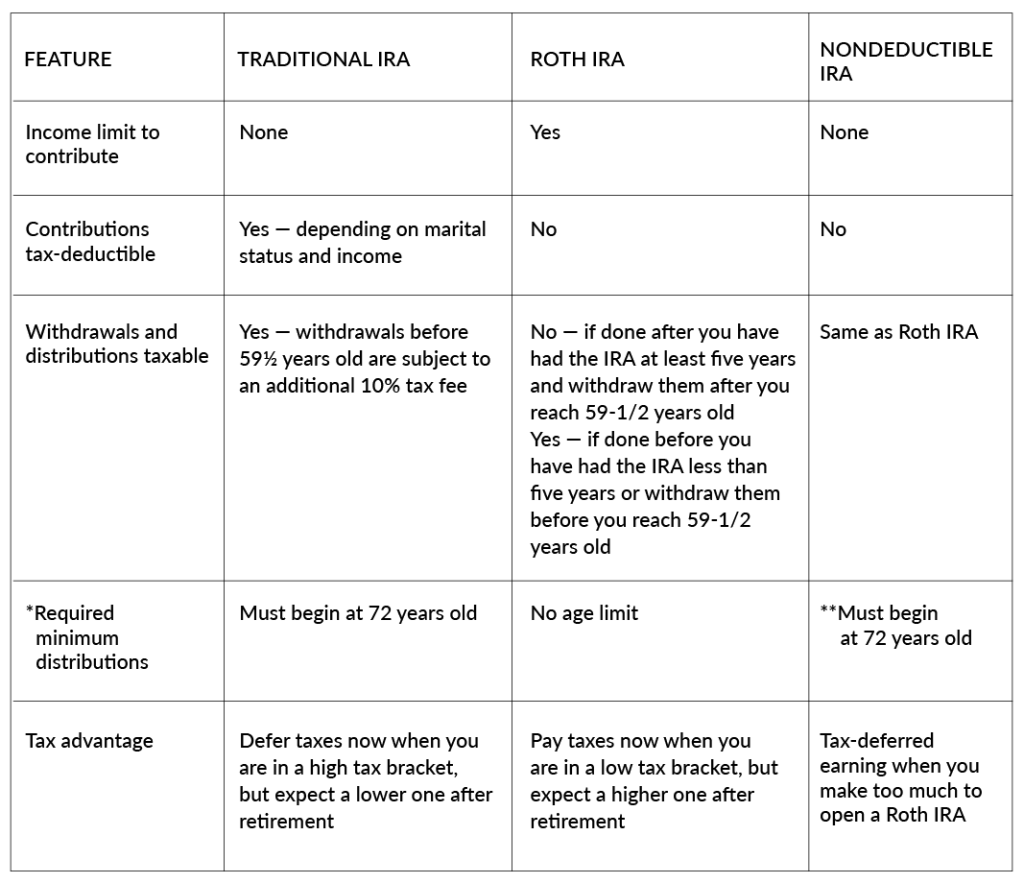

Unlike a Roth IRA, there is no modified adjusted gross income limit to being able to contribute to a traditional IRA, although there are income limits for tax deductible contributions if you have a retirement account from your employer.

Unlike a Roth IRA, there is no modified adjusted gross income limit to being able to contribute to a traditional IRA, although there are income limits for tax deductible contributions if you have a retirement account from your employer.

Like most other retirement accounts, traditional IRA contributions must be made from income earned in the same year as the contribution unless you are rolling over another type of retirement account.

Contributions are usually tax-deductible. If you are in a high tax bracket now, delaying income tax until retirement when your income may be lower makes financial sense. You can claim the tax deduction even if you do not itemize deductions on your tax return.

Whether you can make tax-deductible contributions to your traditional IRA depends on your marital and filing status, whether or not you and/or your spouse have another retirement account from your employer, and your modified adjusted gross income.

You can invest in things other than the traditional ones if you choose a self-directed Roth IRA.

You can invest in things other than the traditional ones if you choose a self-directed Roth IRA.

You can circumvent the income limits by starting with a traditional or nondeductible IRA that has no income limits and convert it to a Roth IRA following specific rules. This is referred to as a Backdoor Roth IRA.

Contributions are not tax deductible; you pay income taxes on your contributions.

- Like a traditional IRA only earned income can be contributed.

- Unlike a traditional IRA:

- Roth IRAs can be funded from many sources such as personal contributions, spousal IRA contributions, transfers from savings, rollover contributions from other retirement accounts, and conversions from other IRA types; and

- You can make contributions to your Roth IRA after you reach age 70½.

- You must report all contributions on an IRS Form 8606.

- You must make any contribution before the IRS tax-filing deadline of April 18 in 2023.

- If you are in a low tax bracket now, paying income tax now rather than at retirement when you might have a higher tax bracket makes financial sense.

Having already paid income tax has many advantages.

- You do not have to have owned the Roth IRA for a specific time before you can withdraw funds, but penalties and income taxes will vary.

- You can withdraw your original contributions whenever you want without penalty or income tax. The IRS will always assume your original contributions come out first when you withdraw money from your Roth IRA.

- You won’t pay income taxes or penalties on the financial gains if you have had the Roth IRA at least five years and withdraw them after you reach 59½ years old.

- If you have reached 59½ years old but haven’t had the account for 5 years, there’s no penalty but you’ll owe income tax on any earnings that you withdraw.

- You will pay a 10% penalty and income tax on any financial gains/earnings withdrawn before 59½ years old, unless the money is used for the same exemptions described in the Traditional IRA section above.

Unlike annuities and employer sponsored retirement plans, there is no limit on how long you can defer withdrawals.

You can arrange to have Roth IRA funds transferred to a living trust so you’re able to use them when you are alive and disperse them as you wish to your beneficiaries after your death.

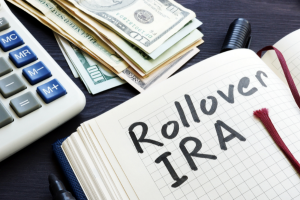

Rollover IRAs are traditional IRAs that receive funds from another retirement account before you can remove money without penalty at 59½ years old. There are advantages of doing this, such as moving money from an employer sponsored to an individual retirement account to have more control over the investments or moving the money to a less restrictive IRA, whether it’s to have easier access to the money or not have income limits.

Rollover IRAs are traditional IRAs that receive funds from another retirement account before you can remove money without penalty at 59½ years old. There are advantages of doing this, such as moving money from an employer sponsored to an individual retirement account to have more control over the investments or moving the money to a less restrictive IRA, whether it’s to have easier access to the money or not have income limits.

Most payments you receive from a retirement plan or IRA before this age can be “rolled over” by depositing the payment in another retirement plan or IRA within 60 days. The money can also be rolled over by having the distribution go directly to the new account. You can roll over all or part of any distribution except:

- Required minimum distributions;

- Loans treated as a distribution;

- Hardship distributions;

- Distributions of excess contributions and related earnings;

- Withdrawals coming from automatic contribution arrangements;

- Distributions to pay for accident, health or life insurance;

- Dividends on employer securities;

- S corporation allocations treated as deemed distributions; or

- A distribution that is one of a series of substantially equal payments.

- This is usually done if you lose your career and therefore your major source of income.

- This basically locks you into taking at least one distribution per year for at least five years or until you turn 591/2, whichever comes last.

- You usually set this up through a financial advisor or directly with your IRA institution.

Tax implications of rollovers can be complicated and best discussed with your agent or plan administrator.

Like an annuity, you may use your retirement as an inheritance tool by naming primary (and possibly contingent) beneficiaries if you die before the end of the retirement account term or it is depleted. The process of naming a beneficiary that is not your spouse is complicated and should be handled by a financial advisor that understands the rules.

Like an annuity, you may use your retirement as an inheritance tool by naming primary (and possibly contingent) beneficiaries if you die before the end of the retirement account term or it is depleted. The process of naming a beneficiary that is not your spouse is complicated and should be handled by a financial advisor that understands the rules.

The primary beneficiary, usually your surviving spouse, will get the money if they claim it. If they have passed away or do not claim the funds, the money then goes to the contingent beneficiaries. Any other beneficiary is free to decline any or all of the account and defer to the next beneficiary. There are three types of beneficiaries:

- Eligible designated beneficiaries, including your spouse and children less than 18 years of age, disabled or chronically ill individuals, and any other individual who is not more than 10 years younger than you at your death;

- Designated beneficiaries are individuals not included in the list above; and

- Not designated beneficiaries, which typically include estates, charities, and trusts.

The beneficiary who accepts the account cannot deposit additional funds and must decide how they’d like to receive their inherited funds. The options available to them are similar to those you had when the retirement account was yours. However, they will need to be aware of some minor differences and a few unique to inherited retirement accounts that will depend on the following factors.

- Whether they are your spouse, a non-spouse or an organization;

- Your age at death;

- Their age in relation to yours at death;

- Their health status; and

- The type of account and any other rules specific to your retirement account.

Options available to beneficiaries of your retirement account

Your surviving spouse can transfer the money from any type of retirement account into their own retirement account. They have 60 days from receiving distribution to do this, as long as the distribution is not a required minimum distribution (RMD). They will then follow the specific rules of the account type based on their age (less than or more than 59½ years old).

- If you had already begun receiving RMDs your surviving spouse must continue to receive the distributions as calculated or submit a new schedule based on their own life expectancy.

- If you had not yet committed to an RMD schedule or reached your required beginning date, your spouse has a five-year window to withdraw the funds, which would then be subject to income taxes.

Your spouse can take over your IRA account and manage it as if it were their own, including the calculation of required minimum distributions. If you have a 401(k) or similar employer sponsored plan it must be rolled over into an inherited IRA.

Your spouse can take over your IRA account and manage it as if it were their own, including the calculation of required minimum distributions. If you have a 401(k) or similar employer sponsored plan it must be rolled over into an inherited IRA.

Since non-spousal beneficiaries of inherited IRAs and 401(k)s or other employer sponsored retirement accounts cannot add inherited account balances to their own, they may have four options.

- Beneficiaries can opt for a lump-sum distribution. This can be split among beneficiaries if there are more than one.

- The withdrawal will not be subject to the usual 10% early withdrawal penalty that you would have paid.

- The money will be taxed that year based on the nature of the account. You will pay income tax for all withdrawals from traditional accounts or on earnings from Roth accounts, but not on the previously taxed contributions.

- Some 401(k) plans will allow these beneficiaries to leave the balance in the plan and take RMDs over their lifetime — this will likely change because of the SECURE Act‘s IRA time limits — or to leave the money in the plan for up to 5 years, during which they must either take distributions or roll the funds into an inherited IRA account.

- The assets continue to grow tax-deferred and can be withdrawn at any time.

- Withdrawals will be taxed that year based on the nature of the account, traditional or Roth.

- Rules for required minimum distributions are similar to those listed above.

- They can name their own beneficiaries for the new account.

- When this option is not available or if they prefer they can roll these accounts into an inherited IRA. Also known as a beneficiary IRA, it is an account specifically opened by any beneficiary, spouse, relative, or unrelated person or entity (estate or trust), to roll over any type of inherited retirement account.

- Rolling over the account avoids the assessment of income taxes when the money is transferred, although beneficiaries must file IRS forms 1099-R and 5498.

- Beneficiaries can opt to have the withdrawals spread out over time. The SECURE Act requires not designated beneficiaries, those who are not your spouse, chronically ill or disabled, less than 10 years older than you, or a minor child to withdraw the entire account by 10 years after inheriting.

- This option gives them flexibility within that time frame to withdraw the money whenever they need it.

- Unless it is a Roth account, this will spread the tax liability over a few years.

- This is probably their best option if a lifetime distribution is not an option.

- There may be a mandatory 20% withholding tax when the money is withdrawn.

- Minor children can spread the withdrawals over the number of years left until their age of maturity.

- Aside from some employer sponsored plans, other designated beneficiaries can spread the withdrawals out over their lifetime.

- Required minimum distributions will start based on your age at the time of death and whether or not you have already started getting them before then.

- Your beneficiary may or may not get notification as to the amount of the required distribution, so they will need to keep track of this to avoid the stiff penalties associated with not taking the required distribution.

- If you were younger than 73 when you died, the surviving spouse must start taking distributions by either the end of the year of your death or the end of the year in which you would have turned 72, whichever date is later.

- If you were older than 72 at the time of your death and not taking withdrawals, your surviving spouse must begin them by the end of the year following your death.

- If you were older than 72 at the time of your death and already taking withdrawals, your surviving spouse must begin them by the end of the year of your death.

- Every year the IRS Single Life Expectancy Table and remaining balance in the account is used to determine the required minimum distribution for that year, although they can withdraw more.

- This continues until there is nothing left in the account or their death, whichever is sooner.

- If a lifetime spread is not offered by your plan, request your employer do a trustee-to-trustee transfer to a retirement account that does.

- Required minimum distributions will start based on your age at the time of death and whether or not you have already started getting them before then.

- Inherited IRAs do not have the same protection from creditors as the original plans did.

- They could name a trust as the beneficiary. The trust can be set up in a way that allows you some control of how the funds are distributed after your death. You would do this for similar reasons as creating any testamentary trust, such as protecting your children from themselves or a step-parent, providing for a disabled child, or donating to a charity.

- The trust can either distribute the account to the beneficiaries (Conduit Trust) or accumulate the payouts and distribute the money to the beneficiaries over a longer period of time (Accumulation Trust).

- Disbursements to individuals from the trust follow the rules for inherited trusts.

- Disbursements to not designated beneficiaries, such as estates, charities, and trusts, are based on your age at the time of your death.

- If you died prior to age 73 the beneficiary must take out the remaining balance over the five-year period following your death.

- If you died after age 73 the beneficiary must take out the remaining balance over your remaining life expectancy.