It can be difficult to keep the various trust options straight. There are a number of ways to look at and compare the different trust choices to help you determine which is best for your situation.

One confusing aspect of trusts is that the name chosen for your trust does not necessarily describe the features and may be an abbreviated version. For example:

- A revocable living trust may be called a revocable trust since testamentary trusts are not revocable and adding ‘living’ is redundant; and

- A trust termed a family trust could be one of many types of trust such as living trust, joint tenancy revocable trust, or testamentary trust, depending on the habits of your estate planner.

Some options presented as types of trust are frequently a combination of the features that you chose for your trust.

Some options presented as types of trust are frequently a combination of the features that you chose for your trust.

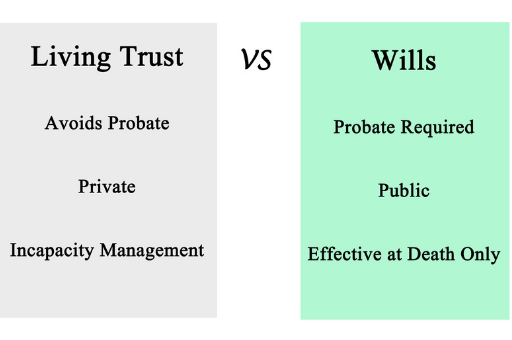

- Do you want the trust to be created and begin to be managed before your death (living trust) or outlined in your will or a living trust to be created after your death (testamentary trust)?

- Are you able to fund it (funded trust) or not (unfunded trust)? A trust is only useful if funded.

If you create a living trust and can fund it, you have three choices to make.

- Do you want to be able to make changes to or close the trust after it is formed (revocable trust) or not be able to close or change the trust (irrevocable trust)?

- Additional features of a revocable living trust:

- You and your revocable trust share the same Social Security number, which is what prompts estate tax.

- The trust’s income and deductions are reported on your personal Form 1040 tax return, as they would if you continued to own the assets personally.

- Trust assets are available to creditors while you are the trustee.

- Additional features of an irrevocable living trust:

- Your irrevocable trust will have its own Social Security number.

- The trust’s income and deductions are reported on a Schedule K-1 (Form 1041).

- Trust assets are protected from creditors and lawsuits against you even while you are alive.

- Trust assets are not subject to estate tax after your death.

- Additional features of a revocable living trust:

- Would you like to manage the trust initially after designating a successor trustee if something happens to you, or appoint another trustee to manage the trust during your lifetime?

- A revocable trust is generally initially managed by you and all irrevocable trusts are managed by another trustee.

- You may have a co-trustee.

- Should you give your trustee emergency power to alter the trust (“Power to Amend Revocable Living Trust Agreement” or a Testamentary Power of Appointment) if needed or not allow it, even at your request?

Additional features to consider.

Additional features to consider.

- Do you want your adult beneficiaries to have control of the assets right after you die or have them managed by a trustee (Discretionary Trust) until they are truly capable of doing so? Discretionary trusts only apply to adult beneficiaries.

- Are you leaving any of your estate to minor children with a trust that exists through the death of your surviving partner (Credit Shelter Trust) or only just until they come of age? Minor children must have a trustee to manage the trust until they are of legal age.

- Do you want to lock in what each minor beneficiary gets with an individual trust or group them together in a Group or Pot Trust to allow the flexibility to adapt to individual needs?

- Do you have dependents with disabilities that will need a Special Needs Trust? Special needs trusts are only appropriate for disabled beneficiaries.

If you create a trust, unless otherwise specified only you can change it. Therefore:

- Living trusts are usually revocable before your death, although you can create an irrevocable living trust, and irrevocable if the trust exists after your death;

- A living trust also becomes irrevocable if you become incapacitated;

- Testamentary trusts are irrevocable as they are formed after your death; and

- If you want to give the trustee the right to alter the trust if you become incapacitated or after your death, you must specifically state such in the trust document or your will if the trust is created in your will.

A family trust is merely a description of any trust going exclusively to family (related by blood, marriage, or law [in the case of adoption] and not a type of trust.

A family trust is merely a description of any trust going exclusively to family (related by blood, marriage, or law [in the case of adoption]) and not a type of trust.

Whatever the type of trust or name given to it, your trust is the sum of all the terms, provisions, and other features it contains. Instead of trying to determine what type of trust you want, determine what features you want the trust or trusts to have.

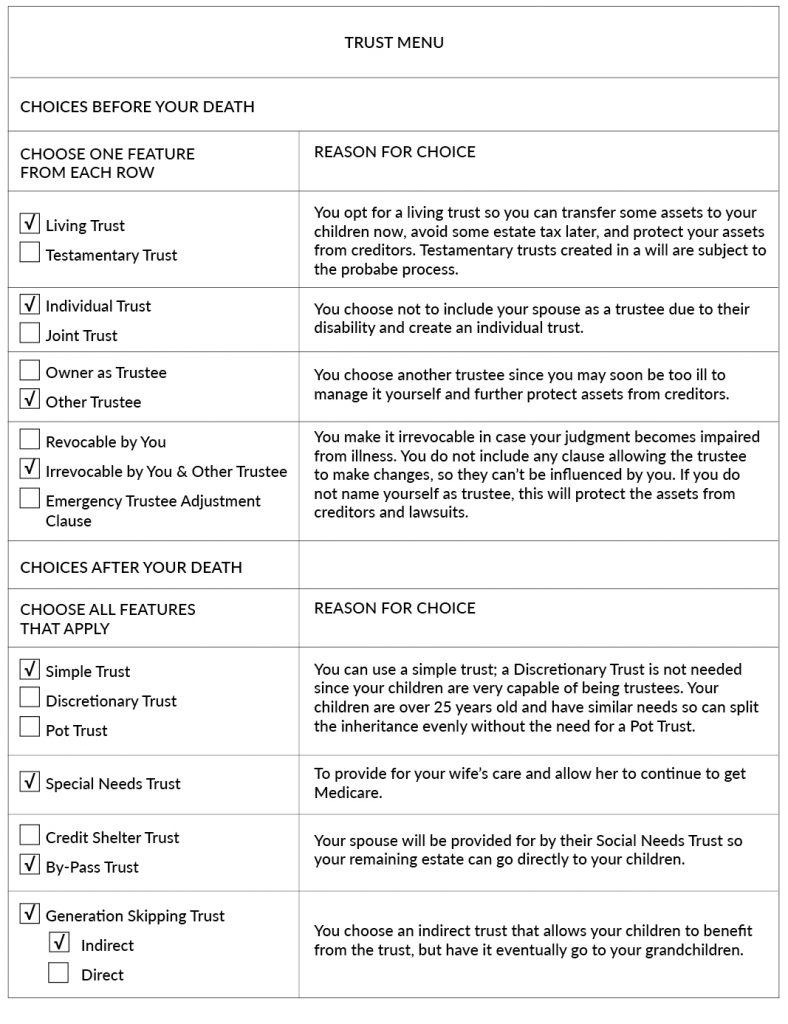

It may be best to think of creating a trust like going through a menu. For example, if you are creating a trust because you are ill and have two adult children with their own children, who are approaching college age, and a disabled spouse, you will be creating a Family Trust since only relatives are included.

It may be best to think of creating a trust like going through a menu. For example, if you are creating a trust because you are ill and have two adult children with their own children, who are approaching college age, and a disabled spouse, you will be creating a Family Trust since only relatives are included.